|

Key News and Trends Impacting Your Local Market

The National Bureau of Economic Research officially deemed February 2020 the most recent U.S. economic peak ending the decade-long expansionary economic cycle, which means we are in a recession until we begin another growth cycle.

During the second quarter of 2020, the GDP—the broadest measure of goods and services produced—dropped 9.5% quarter-over-quarter. GDP and the housing market usually trend together over time. The connection between the two is quite simple: overall personal income should rise as GDP increases, thereby accumulating enough wealth to purchase a home.

Perhaps the more pertinent news regarding GDP is that the federal government offset the drop in production and spending through COVID-19 relief and stimulus measures. Specifically, the recipients of the $600 per week federal unemployment supplement, which ended July 31, largely infused that money back into the economy.

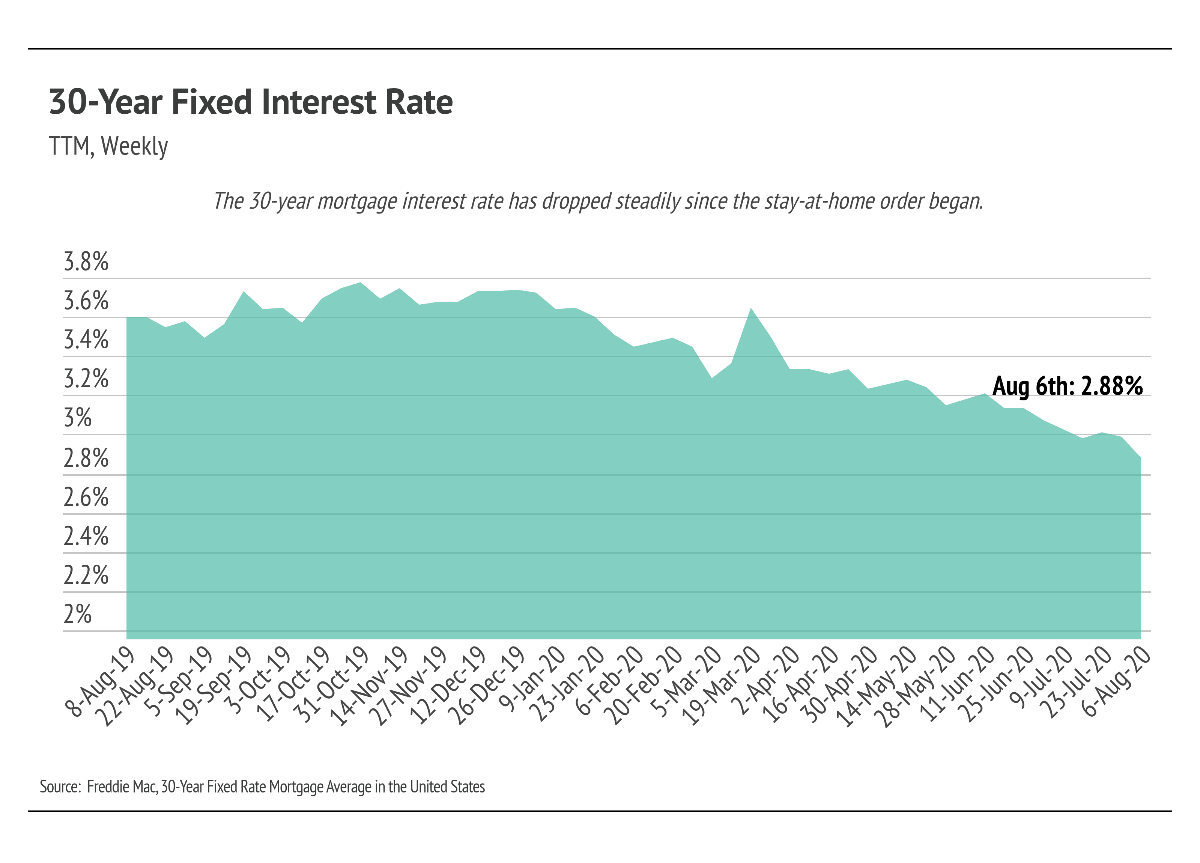

On the other hand, the pandemic has left many with more money than usual as their personal spending has dropped considerably. Those interested and able to buy a home are in the lowest interest rate environment in history. Freddie Mac reports that the interest rate on a 30-year fixed mortgage is at 2.88%. This is the first time the rate has dropped below 3%.

As we have discussed in previous newsletters, the affordability of a home increases (or decreases) significantly with each percentage of interest. A loan for a median-priced home from January 2020 at a rate of 3.72% costs $700 per month more than a loan at 2.88%, amounting to $250,000 over the life of the loan. As a result, we have seen a boom in refinancing, which we expect to continue for homeowners who do not wish to move. For buyers (or refinancers), this could be the lowest interest rate they will experience in their lifetime and an excellent time to execute the purchase of a home.

|